Commentary from the Desk: September 7, 2022

This week, we are closely following:

1. The final lead up to the Merge

2. Our long-term view on ETH supply/demand post-Merge

1. The final lead up to the Merge

If Labor Day weekend officially closed out summer, it also gave us a quick breather before the looming watershed Merge occurs in less than 10 days.

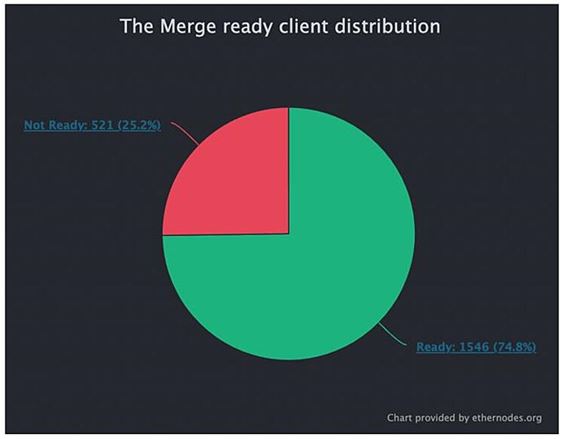

The merge is estimated to occur once the total terminal difficulty (TTD) hits 58,750,000,000,000,000,000,000. This is expected to be between September 12-16. According to Ethernodes, about 74% of Ethereum clients are ready for the Merge.

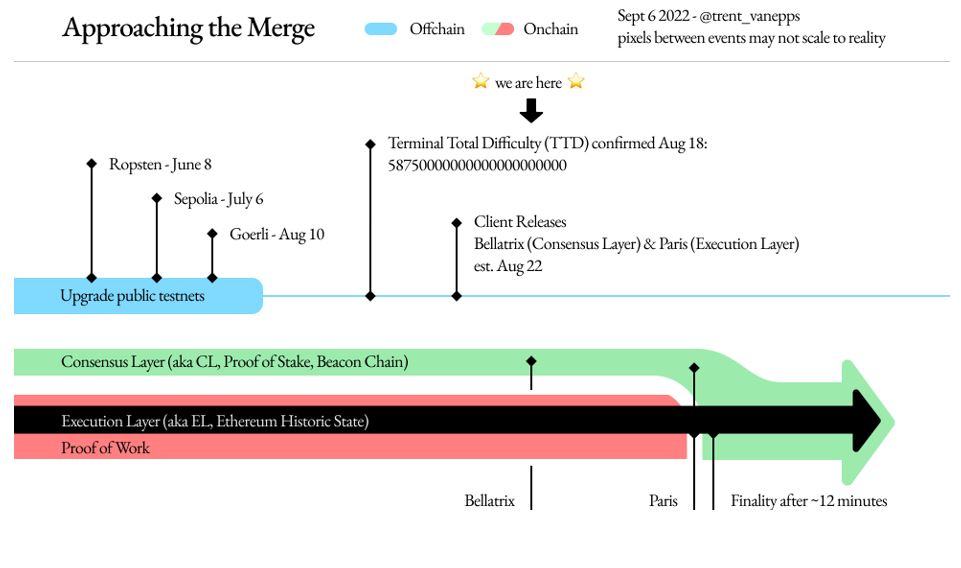

Below is a handy timeline of Merge events pulled together by @trent_vanepps, including all the previous upgrades.

Is the merge priced in?

Is the merge priced in?

This is a popular, yet old, debate. In our view, the merge is not priced in.

The merge is an incredibly challenging feat to accomplish; it’s sometimes compared to swapping the engine of two planes…mid-flight.

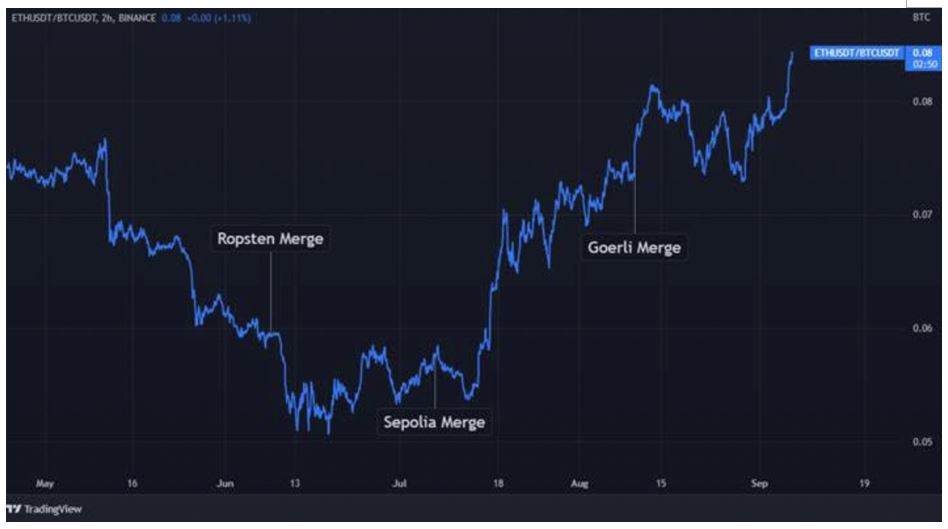

The Ropsten, Sepolia, and Goerli testnet upgrades have all been successful, which made it increasingly clear that the Merge was actually set to occur in the second half of 2022. While all seems to be going according to plan—especially given how technologically challenging of a feat the Merge is—there are no guarantees that it lands on its feet and finishes smoothly.

Indeed, there is a cohort waiting to see if the Merge is successful or not before deploying capital into ETH. Nonetheless, we’ve seen ETH aggressively gaining strength over BTC since mid-July, with ETH/BTC approaching multi-year highs.

If the Merge is successful, but the macroeconomy continues to get worse, does the Merge even matter?

While it's hard to speculate on this while we’re in pre-Merge mode, here is what we do know:

- ETH issuance will decrease substantially;

- The Merge sets the foundations for greater Ethereum scalability;

- Ethereum will become more ESG friendly;

- The Merge, CPI, and FOMC are all within the same week, so brace for volatility;

- July’s headline CPI was flat M/M after rising 1.3% in June, supporting the peak inflation theme, which helped sustain the summer market rally (+0.0% M/M vs. consensus +0.2% and up 8.5% Y/Y, a decline from 9.1% in June), according to Nasdaq Market Intelligence;

- 76% chance of a 75bp rate hike during this month’s FOMC, according to CME FedWatch;

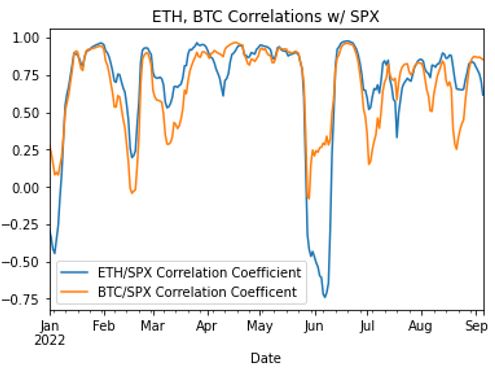

- ETH correlation with the S&P 500 has edged lower, down to 0.615 whereas BTC sits at 0.853.

2. Our long-term view on ETH supply/demand post-Merge

Despite the conflicting factors that will likely create some uncertainty in the short-term, we feel confident that the Merge will ultimately lead to upward price pressure over the long-term.

Adding to our conviction is the growing interest we’ve seen in various bullish options strategies and the dry powder in the form of substantial cash positions following the recent deleveraging of the market.

Overall, we expect to see effective supply fall by about 95% while staking demand increases post-Merge.

Our positive long-term view is based on the following factors:

On the supply side, we see gross inflation falling by ~90% and the ~15% of gas paid to miners/stakers as tip remaining stable. However, effective supply should decline by over 95% since we believe miners sell around 80-90% of mined ETH, whereas we very roughly estimate stakers will only sell ~20% due to substantially lower operating costs.

On the demand side, there are three components:

1. Gas: Currently ~110k ETH per month, with ~85% of which being burned. We assume this remains stable post-Merge, though we think this estimate could be conservative.

2. Staking Demand: Staking in ETH is currently negligible, with the likely cause being that stakers are holding off until post-Merge given the potential technical risk and uncertain timing. Currently, only around 11% of the total supply is staked, which is significantly below the 50-80% average across major PoS L1s. Assuming a conservative total staked ratio of 60%, this could mean an additional 60m of staked ETH at the current supply of ~120m tokens. A reasonable timeframe for this target to be reached is around 16 to 20 months. Although most of this staking demand will end up coming from existing ETH holders, we do expect around 10% net new stakers, attracted by yields that are expected to be above 5%.

3. Speculative Demand: While this is very difficult to estimate, in previous bull markets we have generally seen ~2m ETH per month move from long-term to short-term holders

Therefore, even without any pick-up in speculative demand, we see the supply/demand balance moving from the current situation of slight excess supply to moderate excess demand. This translates to moving from ~260k ETH per month needing to be absorbed by speculative demand, to an excess demand of ~400k ETH per month. This estimate is likely conservative given current cash levels.

There is considerable upside to this if the Merge narrative leads to a sustained pickup in speculative demand. Against this backdrop, around 75% of current supply has not changed hands for around three months. In other words, these tokens are in the hands of quasi long-term holders, which further compounds any potential supply squeeze implied by the below analysis.

Other Going-on ICYMI:

- PWC research predicts a slowdown in crypto interest and investment, particularly retail firms offering coins, tokens and NFTs.

- Vulnerabilities in Crypto Security Have Investors Taking Notice: Bloomberg News

- Crypto miner Hive Blockchain testing other GPU mineable coins ahead of The Merge: The Block

- Crypto firm 21.co raises $25 million to value it at $2 billion: Reuters

- Crypto prices are down, but it’s not scaring away investors—here’s why: CNBC.com

- UK’s Crypto Future in Limbo as Truss Wins Prime Minister Race: Bloomberg News

- Most of the responses to Joe Biden's crypto executive order are due next week: The Block

- Islamic State Turns to NFTs to Spread Terror Message: WSJ

The information (“Information”) provided by Cumberland DRW LLC and its affiliated or related companies (collectively, “Cumberland”), either in this publication or document, or on or through https://cumberland.io/, is for informational purposes only and is provided without charge. Cumberland is not and does not act as a fiduciary or adviser, or in any similar capacity, in providing the Information, and the Information may not be relied upon as investment, financial, legal, tax, regulatory, or any other type of advice. The Information is being distributed as part of Cumberland’s sales and marketing efforts. Cumberland makes no representations or warranties (express or implied) regarding, nor shall it have any responsibility or liability for the accuracy, adequacy, timeliness or completeness of, the Information, and no representation is made or is to be implied that the Information will remain unchanged. Cumberland undertakes no duty to amend, correct, update, or otherwise supplement the Information. In addition, any person wishing to enter into transactions with Cumberland must satisfy Cumberland’s eligibility requirements.

The Information has not been prepared or tailored to address, and may not be suitable or appropriate for the particular financial needs, circumstances or requirements of any person, and it should not be the basis for making any investment or transaction decision. THE INFORMATION IS NOT A RECOMMENDATION TO ENGAGE IN ANY TRANSACTION. The virtual currency industry is subject to a range of risks, including but not limited to: price volatility, limited liquidity, limited and incomplete information regarding certain instruments, products, or cryptoassets, and a still emerging and evolving regulatory environment. The past performance of any instruments, products or cryptoassets addressed in the Information is not a guide to future performance, nor is it a reliable indicator of future results or performance. Investing in virtual currencies involves significant risks and is not appropriate for many investors, including those without significant investment experience and capacity to assume significant risks. Any person seeking to invest in or trade virtual currencies should do so only after engaging in their own research and obtaining their own advice as to whether virtual currencies may be appropriate in the context of their individual circumstances.

Cumberland is a principal trading and market making firm, and Cumberland may be subject to certain conflicts of interest in connection with the provision of the Information. For example, Cumberland may engage in transactions in a manner inconsistent with the views expressed in the Information, and transactions entered into by Cumberland could affect the relevant markets in ways that are adverse to a counterparty of Cumberland. If any person elects to enter into transactions with Cumberland, whether as a result of the Information or otherwise, Cumberland will be acting solely in its own best interests, which may be adverse to the interests of such persons.