Commentary from the Desk: August 17, 2022

This week, we are closely following 3 key developments:

1. Macro (still) in the driver's seat

2. Price action

3. Crypto Updates: Goerli success, Tornado Cash knock-on effects

1. Inflation stays in the (market) driver’s seat

Last week, we picked up some incredibly useful data points regarding inflation with the release of July’s CPI print:

Recapping Headline (i.e., including food and energy):

- CPI rose 8.5% in July from the same month one year ago, which is down from 9.1% in June (June print was the fastest pace of inflation since 1981);

- CPI came in flat MoM, halting an upward trendline over the last 25 months;

- Analyst expectations were roughly 8.7% growth annually and 0.2% monthly, pointing the data in a positive direction;

- Recession fears have eased demand for gas as household budgeting is getting tighter;

- Yield curve remains inverted with the 10-yr sitting at 2.913% and the 2-yr sitting at 3.343%

Recapping Core (i.e., excluding food and energy)

- Core CPI rose 5.9% annually and 0.3% monthly, compared to estimates of 6.1% and 0.5%, respectively;

- This data nods towards inflation potentially peaking; however, one good print doesn’t create a trend. The Fed will be looking for consecutive months of slowed growth before they stop tightening;

Headline decreases were mostly due to falling energy prices (-4.6% MoM and Gasoline -7.7%). In an uncertain geopolitical environment (i.e., Russia’s invasion of Ukraine and other global developments), this can be reversed with increased tensions.

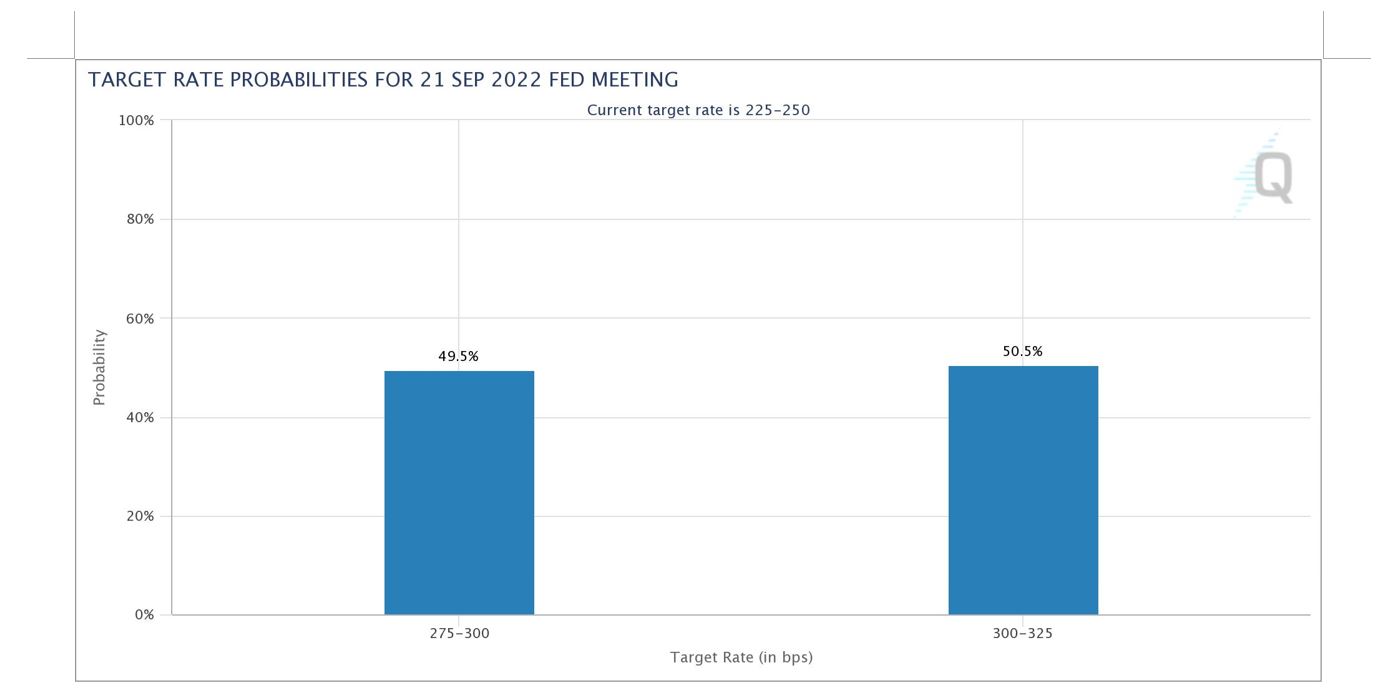

Further, according to CME Group’s FedWatch tool, the probability of the Fed raising interest rates by either 50bps or 75bps is split 49.5% and 50.5%, respectively.

In other macro news, the NY Fed Empire State Manufacturing Index fell to -31.3 indicating a contraction in business conditions, and US housing starts fell 9.6% in July.

The main takeaways here are:

- Inflation risk seems to have subsided significantly, and that can be seen in 10yr bond-yield

- Although the former may be positive, recessions are not good for equities or retail demand. The S&P 500 is currently trading at 17-18x P/E and is already close to Goldman Sachs’ EOY price target of $4,300. Additionally, with crypto being highly correlated with traditional markets, the situation currently looks like a mixed bag.

2. Price Action

- Broader indices: SPX up to $4,272 from $3,650 in mid-July, NDX up to $13,453 from $11,050 mid-July

- Crypto: BTC has lagged ETH, up only 12.4% in the last 30 days vs ETH up 36% in the last 30 days

- The final testnet (Goerli) for the upcoming Ethereum Merge was successful last week

- Tokens benefiting from the upcoming Merge have rallied (e.g. OP, MATIC, LDO, etc.), but some have shaved off gains as of recent with OP down 16.7% in the last 7 days).

3. Crypto Updates: Goerli success, Tornado Cash Knock-on effects

Once again, the big idiosyncratic catalyst remains the upcoming Ethereum Merge. As we discussed last week, the Goerli testnet was successful, thus teeing up what looks to be a successful September Merge.

Current rumblings around the potential PoW fork haven’t increased in tenor or traction. This doesn’t discount it not happening; however, major projects have been—and remain—vocally supportive of the PoS chain.

In other developments, since the OFAC’s sanction of Tornado Cash, the news cycle around has continued at full-steam. Last Wednesday, the Dutch police arrested a suspected Tornado Cash developer in Amsterdam.

Tornado Cash has been a useful tool for hackers to launder money, for example:

- Ronin bridge: $455m

- Harmony bridge: $100m

- Over $2bn has been stolen across 13 separate chains according to Chainalysis

While the front-end has been taken down, the Tornado Cash smart contracts are immutable and exist on-chain, so they can still be leveraged.

What are the implications for DeFi protocols?

- USDC is getting frozen due to sanctions, which some DeFi protocols seem to be getting worried about;

º NB: Over 50% of Dai’s reserves are USDC;

º Founder of MakerDao, Rune Christensen, said Dai should “seriously consider preparing to depeg from USDC”; - Protocols have been flagging users that aren’t compliant with OFAC sanctions, including blocking them from accessing the protocol front-end.

The kicker: Regulation has been a looming crypto headwind for years. Now with OFAC taking severe measures (read: sanctioning) this could further drive momentum for similar action by the world’s governments and regulators.

Other Going-on ICYMI:

- Genesis CEO, Michael Moro, steps down as the firm lays off 20% of its staff. Genesis, a core business of Digital Currency Group, was the largest lender to Three Arrows Capital.

- Do Kwon, founder of Luna, which played an integral role in the crypto market downturn, breaks his silence.

- CoinFund, founded by Jake Brukhman in 2015, raises a $300m Web3 fund to invest in early-stage crypto projects. Previously, the firm has been an early-stage investor in projects/companies such as Rarible, Balancer, Messari, and more.

- Chicago-based Jump Crypto and the Solana Foundation are working on developing a second validator client for the Solana Network. Jump played an integral role in the development of Solana and its ecosystem, and while Solana is notorious for its frequent outages, this is a big step in increasing the network’s reliability

- Injective raises $40m from Jump and Brevan Howard Digital

“The information (“Information”) provided by Cumberland DRW LLC and its affiliated or related companies (collectively, “Cumberland”), either in this publication or document, or on or through https://cumberland.io/, is for informational purposes only and is provided without charge. Cumberland is not and does not act as a fiduciary or adviser, or in any similar capacity, in providing the Information, and the Information may not be relied upon as investment, financial, legal, tax, regulatory, or any other type of advice. The Information is being distributed as part of Cumberland’s sales and marketing efforts. Cumberland makes no representations or warranties (express or implied) regarding, nor shall it have any responsibility or liability for the accuracy, adequacy, timeliness or completeness of, the Information, and no representation is made or is to be implied that the Information will remain unchanged. Cumberland undertakes no duty to amend, correct, update, or otherwise supplement the Information. In addition, any person wishing to enter into transactions with Cumberland must satisfy Cumberland’s eligibility requirements. The

Information has not been prepared or tailored to address, and may not be suitable or appropriate for the particular financial needs, circumstances or requirements of any person, and it should not be the basis for making any investment or transaction decision. THE INFORMATION IS NOT A RECOMMENDATION TO ENGAGE IN ANY TRANSACTION. The virtual currency industry is subject to a range of risks, including but not limited to: price volatility, limited liquidity, limited and incomplete information regarding certain instruments, products, or cryptoassets, and a still emerging and evolving regulatory environment. The past performance of any instruments, products or cryptoassets addressed in the Information is not a guide to future performance, nor is it a reliable indicator of future results or performance. Investing in virtual currencies involves significant risks and is not appropriate for many investors, including those without significant investment experience and capacity to assume significant risks. Any person seeking to invest in or trade virtual currencies should do so only after engaging in their own research and obtaining their own advice as to whether virtual currencies may be appropriate in the context of their individual circumstances.

Cumberland is a principal trading and market making firm, and Cumberland may be subject to certain conflicts of interest in connection with the provision of the Information. For example, Cumberland may engage in transactions in a manner inconsistent with the views expressed in the Information, and transactions entered into by Cumberland could affect the relevant markets in ways that are adverse to a counterparty of Cumberland. If any person elects to enter into transactions with Cumberland, whether as a result of the Information or otherwise, Cumberland will be acting solely in its own best interests, which may be adverse to the interests of such persons.”